CALL US TODAY: (870) 425-4300

If you've been following the news recently, you might have seen articles about an increase in foreclosures and bankruptcies. That could be making you feel uneasy, especially if you're thinking about buying or selling a house.

But the truth is, even though the numbers are going up, the data shows the housing market isn’t headed for a crisis.

In recent years, the number of foreclosures has been very low. That’s because, in 2020 and 2021, the forbearance program and other relief options were put in place to help many homeowners stay in their homes during that tough time.

When the moratorium ended, there was an expected rise in foreclosures. But just because they’re up, that doesn't mean the housing market is in trouble.

To help you see how much things have changed since the housing crash in 2008, check out the graph below using research from ATTOM, a property data provider. It looks at properties with a foreclosure filing going all the way back to 2005 to show that there have been fewer foreclosures since the crash.

As you can see, foreclosure filings are inching back up to pre-pandemic numbers, but they're still way lower than when the housing market crashed in 2008. And today, the tremendous amount of equity American homeowners have in their homes can help people sell and avoid foreclosure.

As you can see below, the financial trouble many industries and small businesses felt during the pandemic didn’t cause a dramatic increase in bankruptcies. Still, the number of bankruptcies has gone up slightly since last year, nearly returning to 2021 levels. But that isn’t cause for alarm.

The numbers for 2021 and 2022 were lower than more typical years. That’s in part because the government provided trillions of dollars in aid to individuals and businesses during the pandemic. So, let’s instead focus on the bar for this year and compare it to the bar on the far left (2019). It shows the number of bankruptcies today is still nowhere near where it was before the pandemic. Both of these two factors are reasons why the housing market isn't in danger of crashing.

Right now, it's crucial to understand the data. Foreclosures and bankruptcies are rising, but these leading indicators aren’t signaling trouble that would cause another crash.

Do negative headlines and talk on social media have you feeling worried about the housing market? Maybe you’ve even seen or heard something lately that scares you and makes you wonder if you should still buy or sell a home right now.

Regrettably, when news in the media isn't easy to understand, it can make people feel scared and unsure. Similarly, negative talk on social media spreads fast and creates fear. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You should lean on a trusted real estate agent to help you separate fact from fiction and get the answers you need.

That agent will use their knowledge of what’s really happening with home prices, housing supply, expert forecasts, and more to give you the best possible advice. The National Association of Realtors (NAR) explains:

“. . . agents combat uncertainty and fear with a combination of historical perspective, training and facts.”

The right agent will help you figure out what’s going on at the national level and in your local area.

They’ll debunk headlines using data you can trust. Plus, they have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

If you need reliable information about the housing market and expert advice about your own move, let’s connect. 870-425-4300.

When it comes to selling your house, you’re probably trying to juggle the current market conditions and your own needs as you plan your move.

One thing that may be working in your favor is how few homes there are for sale right now. Here’s what you need to know about the current inventory situation and what it means for you.

When you’re selling something, it helps if what you’re selling is in demand, but is also in low supply. Why? That makes it even more desirable since there’s not enough to go around. That’s exactly what’s happening in the housing market today. There are more buyers looking to buy than there are homes for sale.

To tell the story of just how low inventory is, here’s the latest information on active listings, or homes available for sale. The graph below uses data from Realtor.com to show how many active listings there were in September of this year compared to what’s more typical in the market.

As you can see in the graph, if you look at the last normal years for the market (shown in the blue bars) versus the latest numbers for this year (shown in the red bar), it’s clear inventory is still far lower than the norm.

Buyers have fewer choices now than they did in more typical years. And that’s why you could still see some great perks if you sell today. Because there aren’t enough homes to go around, homes that are priced right are still selling fast and the average seller is getting multiple offers from eager buyers. Based on the latest data from the Confidence Index from the National Association of Realtors (NAR):

An article from Realtor.com also explains how the limited number of houses for sale benefits you if you’re selling:

“. . . homes spent two weeks less on the market this past month than they did in the average September from 2017 to 2019 . . . as still-limited supply spurs homebuyers to act quickly . . .”

Because the supply of homes for sale is so low, buyers desperately want more options – and your house may be just what they’re looking for. Let’s connect to get your house listed at the right price for today’s market. You could still see it sell quickly and potentially get multiple offers. 870-425-4300.

If you've ever dreamed of buying your own place, or selling your current house to upgrade, you're no stranger to the rollercoaster of emotions changing home prices can stir up. It's a tale of financial goals, doubts, and a dash of anxiety that many have been through.

But if you put off moving because you’re worried home prices might drop, make no mistake, they’re not going down. In fact, it's just the opposite. National data from several sources says they’ve been going up consistently this year (see graph below):

Here’s what this graph shows. In the first half of 2022, home prices rose significantly (the green bars on the left side of the graphs above). Those increases were dramatic and unsustainable.

So, in the second half of the year, prices went through a correction and started dipping a bit (shown in red). But those slight declines were shallow and short-lived. Still, the media really focused on those drops in their headlines – and that created a lot of fear and uncertainty among consumers.

But here’s what hasn’t been covered fully. So far in 2023, prices are going up once more, but this time at a more normal pace (the green bars on the right side of the graphs above). And after price gains that were too high and then the corrections that followed in 2022, the fact that all three reports show more normal or typical price appreciation this year is good news for the housing market.

Orphe Divounguy, Senior Economist at Zillow, explains changing home prices over the past 12 months this way:

“The U.S. housing market has surged over the past year after a temporary hiccup from July 2022-January 2023. . . . That downturn has proven to be short lived as housing has rebounded impressively so far in 2023. . .”

Looking ahead, home price appreciation typically starts to ease up this time of year. As that happens, there’s some risk the media will confuse slowing price growth (deceleration of appreciation) with home prices falling (depreciation). Don’t be fooled. Slower price growth is still growth.

One reason why home prices are going back up is because there still aren't enough homes for sale for all the people who want to buy them.

Even though higher mortgage rates cause buyer demand to moderate, they also cause the supply of available homes to go down. That’s because of the mortgage rate lock-in effect. When rates rise, some homeowners are reluctant to sell and lose their current low mortgage rate just to take on a higher one for their next home.

So, with higher mortgage rates impacting both buyers and sellers, the supply and demand equation of the housing market has been affected. But since there are still more people who want to purchase homes than there are homes available to buy, prices continue to rise. As Freddie Mac states:

“While rising interest rates have reduced affordability—and therefore demand—they have also reduced supply through the mortgage rate lock-in effect. Overall, it appears the reduction in supply has outweighed the decrease in demand, thus house prices have started to increase . . .”

If you put off moving because you were worried that home prices might go down, data shows they’re increasing across the country. Let’s connect so you can understand how home prices are changing in our local area. Call us at 870-425-4300 or go to our Agents page to connect with any one of our fine REALTOR® agents.

Are you thinking about selling your house as a For Sale by Owner (FSBO)? If so, know there's a whole lot more time and expertise needed in that process than you might think. While the idea of doing it all by yourself might seem tempting, it's important to recognize the challenges you may face if you take it on all by yourself. As a recent article from Bankrate explains:

“Choosing the right price, crafting a compelling listing, marketing to potential buyers, coordinating showings, preparing paperwork: All of these are tasks that, in the absence of a real estate agent, you will have to do yourself.”

Here’s a bit more information on just a few of those things and how you may miss out if you don’t use an agent.

Pricing your house right is key to a successful sale. Real estate agents have experience navigating this housing market and understand the art of pricing a home to sell today. Unfortunately, homeowners who sell on their own often lack this all-important experience. That can lead to two common consequences: overpricing or underpricing the house.

An article from Nerd Wallet offers this advice:

“If your home is overpriced, you run the risk of buyers not seeing the listing. . . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

Don’t run this risk. Instead, partner with an agent to make sure your house is priced at current market value, so it catches the eyes of eager buyers. This will put your house in a position to make the best first impression possible.

In this digital age, online marketing has become a real game-changer, especially when it comes to selling your house. A recent report from the National Association of Realtors (NAR), explains:

“Among all generations of home buyers, the first step taken in the home search process was to look online for properties.”

When you partner with a real estate agent who knows how to take advantage of online marketing tools and resources, you'll be able to get in front of these tech-savvy house hunters, boosting your chances of a successful sale. But, if you're attempting to sell your house on your own, you might find yourself missing out on the full power of online and social media strategies.

When you decide to sell your house, you're not just on a quest to find a buyer; you're also stepping into a world of negotiations. You’ll have to coordinate with a bunch of people, including the buyer, the buyer’s agent, the inspection company, the appraiser, and more. It's a dance where every move counts, and the expertise of a real estate agent can make a world of difference in keeping these negotiations on track and sealing the deal.

As NerdWallet says:

“Your listing agent will also, of course, be on your side throughout negotiations. They'll double-check paperwork that comes through, communicate with the buyer's agent and other parties to the sale, and generally stay on top of things through to closing day.”

If you're thinking about selling your house and the idea of going it alone has crossed your mind, be sure to think through that decision carefully. Let's connect to discuss how a real estate agent has the experience needed to take all that stress off your plate.

Mortgage rates have been back on the rise recently and that’s getting a lot of attention from the press. If you’ve been following the headlines, you may have even seen rates recently reached their highest level in over two decades (see graph below):

That can feel like a little bit of a gut punch if you’re thinking about making a move. If you’re wondering whether or not you should delay your plans, here’s what you really need to know.

There’s no denying mortgage rates are higher right now than they were in recent years. And, when rates are up, that affects overall home affordability. It works like this. The higher the rate, the more expensive it is to borrow money when you buy a home. That’s because, as rates trend up, your monthly mortgage payment for your future home loan also increases.

Urban Institute explains how this is impacting buyers and sellers right now:

“When mortgage rates go up, monthly housing payments on new purchases also increase. For potential buyers, increased monthly payments can reduce the share of available affordable homes . . . Additionally, higher interest rates mean fewer homes on the market, as existing homeowners have an incentive to hold on to their home to keep their low interest rate.”

Basically, some people are deciding to put their plans on hold because of where mortgage rates are right now. But what you want to know is: is that a good strategy?

If you’re eager for mortgage rates to drop, you’re not alone. A lot of people are waiting for that to happen. But here’s the thing. No one knows when it will. Even the experts can’t say with certainty what’s going to happen next.

Forecasts project rates will fall in the months ahead, but what the latest data says is that rates have been climbing lately. This disconnect shows just how tricky mortgage rates are to project.

The best advice for your move is this: don’t try to control what you can’t control. This includes trying to time the market or guess what the future holds for mortgage rates. As CBS News states:

“If you're in the market for a new home, experts typically recommend focusing your search on the right home purchase — not the interest rate environment.”

Instead, work on building a team of skilled professionals, including a trusted lender and real estate agent, who can explain what’s happening in the market and what it means for you. If you need to move because you’re changing jobs, want to be closer to family, or are in the middle of another big life change, the right team can help you achieve your goal, even now.

The best advice for your move is: don’t try to control what you can’t control – especially mortgage rates. Even the experts can’t say for certain where they’ll go from here. Instead, focus on building a team of trusted professionals who can keep you informed. When you’re ready to get the process started, let’s connect.

Take a moment to imagine where you want to be in a few years. You might be thinking about your job, money, wanting more stability, or goals you want to reach soon. Is homeownership a part of that vision? If it is, you should know owning a home has a whole lot of financial benefits.

One of the many reasons to buy a home is that it’s a great way to build wealth and gain financial stability. That’s because the value of most homes increases over time, which in turn grows your net worth. Here’s how home values are rising right now. According to Zillow:

“The total value of the U.S. housing market – the sum of Zillow’s estimated value for every U.S. home – is now slightly less than $52 trillion, which is $1.1 trillion higher than the previous peak reached last June.”

Basically, homeownership is a tremendous wealth-building tool. And with home values back on the rise across the nation, now might be a good time to consider if owning a home is something you want to reach for.

Here’s a look at some data to see how much owning a home can really make a difference in your life.

Data shows that while those in the top 1% saw the most dramatic net worth increase, people from every single tax bracket have seen their wealth grow over the past few years (see graph below):

For many of those people, the rising value of their home plays a big part in that.

You can tell homeownership had a lot to do with that growth because there’s a significant net worth gap between homeowners and renters. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“. . . homeownership is a catalyst for building wealth for people from all walks of life. A monthly mortgage payment is often considered a forced savings account that helps homeowners build a net worth about 40 times higher than that of a renter.”

The big reason why? Homeowner’s build equity. Home equity is the value of your home minus the amount you owe on your mortgage. And for most homeowners, that’s the largest contributor to their net worth. Here’s the data from First American to prove it (see graph below):

The blue portion of each bar represents housing as a portion of net worth – and it’s clearly a bigger contributor than other investments like stocks, gold, and cryptocurrencies. As you can see, across different income levels, homeownership does more to build the average household’s wealth than anything else.

One of the biggest benefits of owning a home is that it can provide an avenue to grow your net worth. Let’s connect so you can start investing in homeownership.

Are you thinking about making a move? If so, all the speculation that home prices would crash this year may have you feeling a bit on edge about your decision. Let the data and the experts reassure you. Prices aren’t in a downward spiral and will actually finish the year strong.

Even though you may have heard talk that prices would drop 5, 10, or even 20% this year, that hasn’t happened. The big reason why is the supply of homes for sale is too low. There are just more buyers looking to buy than homes available, and that’s kept prices from falling.

To prove this year wasn’t a bust for home prices, let’s look at the latest 2023 forecast from a number of experts.

The general consensus from industry experts is that home price appreciation will actually be positive for 2023. The graph below shows the latest 2023 year-end forecasts from six different organizations:

As you can see, all but one project nationally prices will net positive this year. That’s significant because it shows the majority are optimistic about home price growth.

If you’re still worried about the one red bar that shows an overall price drop for the year, think about this. The projection from the National Association of Realtors (NAR) is for only a slight decline. It’s not the big crash all the headlines called for. Plus, if you average all six forecasts together, the expectation is that prices will net somewhere around 3.3% positive growth for the year.

If these 6 organizations aren’t enough to convince you that prices won’t come tumbling down, here’s something else to consider. One of the six forecasts represented in the graph is the Home Price Expectation Survey (HPES) from Pulsenomics. It combines survey results from over 100 economists, investment strategists, and housing market analysts. The HPES found that the average from all 100 of those experts is 3.3% price growth for the year.

If you look back at the graph above, you’ll notice the blue average for the forecasts in this graph is also 3.3%. While individual forecasts may vary, both the HPES survey and the average of these forecasts provide the same projection. And 3.3% appreciation is a completely different story than prices falling.

If you’re worried about home prices falling this year, let the experts reassure you. Based on the average of the latest forecasts, home prices will actually show positive growth this year. If you have questions about what’s happening with home prices in our local area, let’s connect. 870-425-4300.

During the pandemic, many people distanced themselves from their loved ones for health reasons. Grandparents were told to stay away from their grandkids, especially as schools started to open. That’s because it would have been risky to visit with their grandchildren who may have gotten sick from school.

Now that the pandemic has passed, many grandparents want more than ever to be near their grandchildren again to make up for that lost time. But how are they getting that “Grandparent Wish?” The data tells us many are moving to make sure they’re getting more quality time.

Recent data from the National Association of Realtors (NAR) shows people between the ages of 55 and 74 are moving farther (more than 100 miles) than any other age group (see graph below):

The average age of grandparents in the U.S. is 67 years. The logical leap is that at least some of the people who are moving the furthest are grandparents. But what’s causing them to move so far?

The same report from NAR shows the top reason people move is to be closer to loved ones (see graph below):

Based on this data, it’s fair to say many grandparents are getting their wish of more quality time with their grandchildren by moving to be closer to them. And after experiencing isolation and loneliness during the COVID pandemic, that’s an especially good thing.

If you’re a grandparent, you know how important your grandchildren are. And you may be willing to sell and move just to be closer by. As Vance Cariaga, a journalist at Go Bank Rates, explains:

“Never underestimate the power of grandchildren – especially when it comes to lifestyle and financial decisions. Recent data shows that many baby boomers are relocating further away from home than they used to so they can be closer to their grandbabies.”

The data shows grandparents are moving further to be near their grandchildren. If you have grandchildren of your own, maybe you can relate. When you decide it’s time to be closer to your loved ones, let's connect.

Are you considering buying your first home? If so, it can be helpful to know what led other people to make that decision. According to a recent survey of first-time homebuyers by PulteGroup:

“When asked why they purchased their first home recently, the answer was simple: because they wanted to. Either the desire to stop renting or recognition that homeownership is a smart financial investment was the main motivator for 72% of respondents.”

While that survey looked specifically at first-time homebuyers buying newly built homes, the same sentiment is true for just about anyone buying their first home. Here’s a bit more information to help you think about those two benefits of homeownership to see if they’re a key factor for you too.

You might want to stop renting because rents keep going up. If you’re a renter, that means there’s a chance your payment will increase each time you sign a new rental agreement or renew your current one.

On the other hand, when you buy your home with a fixed-rate mortgage, your monthly housing payment is predictable over the length of that loan. This stability can give you a peace of mind that renting just can’t provide. Jeff Ostrowski, real estate journalist, breaks it down:

“With a fixed-rate mortgage, your monthly principal and interest payment is set for as long as you keep the loan. Sign a rental lease, however, and you could see your rent rise the following year, the year after that and so on.”

Beyond that, owning a home can also be a great long-term investment. While renting may be the more affordable option right now, it doesn’t provide an avenue for you to grow your wealth over time. Mark Fleming, Chief Economist at First American, explains that’s an important distinction to consider:

“Given current dynamics, more young households may choose to rent in the near term as the cost to own, excluding house price appreciation, has unequivocally increased. Yet, accounting for house price appreciation in that cost of homeownership, whether to rent or buy will depend on where, and if, a home is likely to cost more or less in the near future.”

Basically, renting doesn’t allow you to build equity. In contrast, homeownership can help you grow your net worth as your home’s value appreciates. That’s a significant perk you can’t get if you keep renting.

When you take that into account, it may make better financial sense to buy. Most experts project home prices will continue to appreciate over the next few years at a pace that’s more normal for the market. That means when you buy a home, not only are you investing in a place to live, but you’re also investing in your financial future.

If you're ready, it can be a smart move to buy your first home instead of renting. Let’s connect so you can stabilize your housing payment and start building wealth for your future. 870-425-4300

During the fourth quarter of last year, some housing experts projected home prices were going to crash in 2023. The media ran with those forecasts and put out headlines calling for doom and gloom in the housing market. All of this negative news coverage made a lot of people have doubts about the strength of the residential real estate market.

If it made you question if you should delay your own plans to move, here’s what you really need to know.

Disregard what you saw in the headlines. The actual data shows home prices were remarkably resilient and performed far better than the media would have you believe (see graph below):

This graph uses reports from three trusted sources to clearly illustrate prices have already rebounded after experiencing only slight declines nationally. That’s a far cry from the crash so many articles called for.

The declines that did happen (shown in red), weren’t drastic but were short-lived. As Nicole Friedman, a reporter at the Wall Street Journal (WSJ), says:

“Home prices aren’t falling anymore. . . The surprisingly quick recovery suggests that the residential real-estate downturn is turning out to be shorter and shallower than many housing economists expected . . .”

Even though some media coverage made a big deal about home prices pulling back, the slight correction that happened is already in the rearview mirror. Basically, this data shows you home prices aren’t falling anymore – they’re actually going back up.

The consensus from experts is that home price growth will continue in the years ahead and is returning to normal levels for the market. That means we’ll still see home prices appreciating, just at a slower pace than the last few years – and that’s a good thing.

Some news sources will see home price growth slowing and put out stories that make you think prices are falling again. The return of misleading headlines like those is already having an impact on how homebuyers are feeling again. You can see how this affects general opinion in the Consumer Confidence Survey from Fannie Mae (see graph below):

While the percentage of Americans who think prices will fall has been slowly declining this year, the latest Consumer Confidence data indicates that’s ticked back up recently (shown in red). This change is surprising especially since the home price data shows prices are going up, not down. It tells you the impact the media still has on public opinion.

Don’t fall for the negative headlines and become part of this statistic. Remember, data from a number of sources shows home prices aren’t falling anymore.

Even though the media may make things sound doom and gloom, the data shows home prices aren’t falling anymore. So, don’t let the headlines scare you or delay your plans. Let's connect so you have a trusted resource to cut through the noise and tell you what’s really happening in our area. 870-425-4300.

If you’re thinking about buying a home soon, higher mortgage rates, rising home prices, and ongoing affordability concerns may make you wonder if it still makes sense to buy a home right now. While those market factors are important, there's more to consider. You should think about the long-term benefits of homeownership too.

Think about this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how home values grow with time and how, by extension, that grows your own wealth. That may be why, in a recent Fannie Mae survey, 76% of respondents say they believe buying a home is a safe investment.

Here’s a look at how just the home price appreciation piece can really add up over the years.

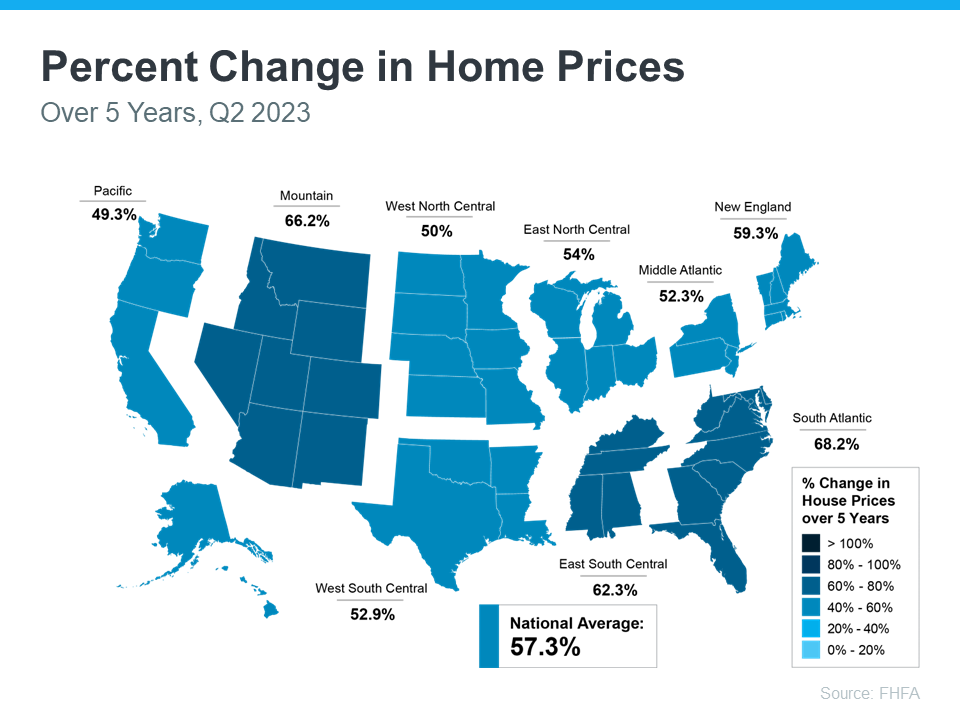

The map below uses data from the Federal Housing Finance Agency (FHFA) to show just how noteworthy price gains have been over the last five years. And, since home prices vary by area, the map is broken out regionally to help convey larger market trends:

If you look at the percent change in home prices, you can see home prices grew on average by just over 57% nationwide over a five-year period.

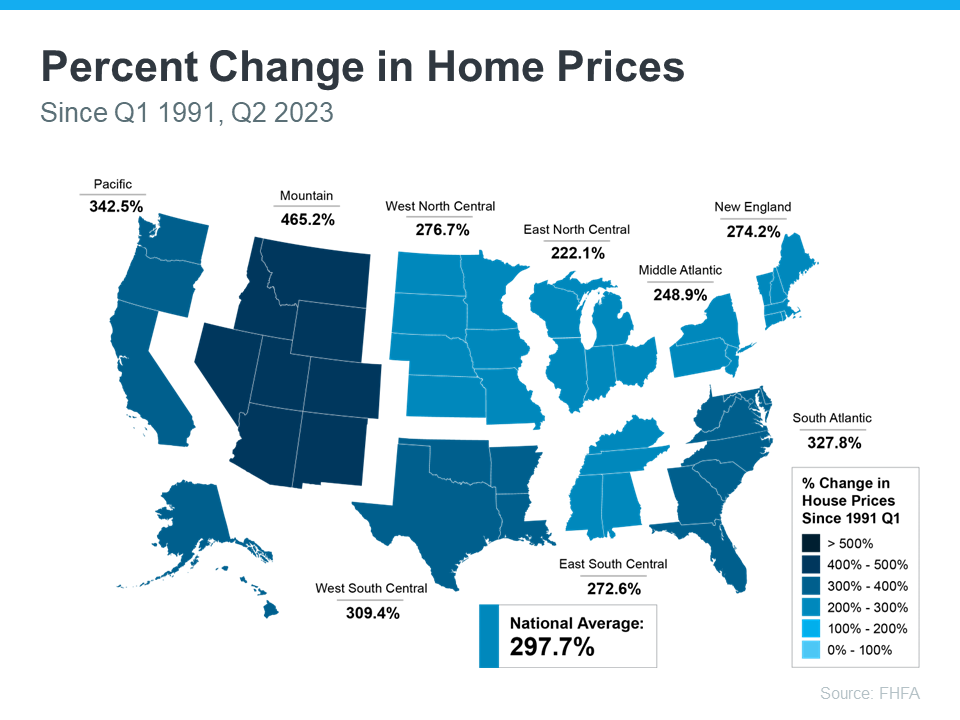

Some regions are slightly above or below that average, but overall, home prices gained solid ground in a short time. And if you expand that time frame even more, the benefit of homeownership and the drastic gains homeowners made over the years become even clearer (see map below):

The second map shows, nationwide, home prices appreciated by an average of over 297% over a roughly 30-year span.

This nationwide average tells you the typical homeowner who bought a house 30 years ago saw their home almost triple in value over that time. That’s a key factor in why so many homeowners who bought their homes years ago are still happy with their decision.

And while you may have heard talk throughout the year that home prices would crash, it hasn’t happened. In fact, experts project home prices will continue to rise for years to come.

If you’re wondering if it still makes sense to buy a home today, it's important to focus on the long-term advantages that come with homeownership. When you’re ready to start your homebuying journey, let’s chat. 870-425-4300.