CALL US TODAY: (870) 425-4300

It’s economy 101 – when supply is low and demand is high, prices naturally rise. That’s what’s happening in today’s housing market. Home prices are appreciating at near-historic rates, and that’s creating some challenges when it comes to home appraisals.

In recent months, it’s become increasingly common for an appraisal to come in below the contract price on the house. Shawn Telford, Chief Appraiser for CoreLogic, explains it like this:

“Recently, we observed buyers paying prices above listing price and higher than the market data available to appraisers can support. This difference is known as ‘the appraisal gap . . . .’”

Basically, with the heightened buyer demand, purchasers are often willing to pay over asking to secure the home of their dreams. If you’ve ever toured a house you’ve fallen in love with, you understand. Once you start to picture yourself and your furniture in the rooms, you want to do everything you can to land the property, including putting in a high offer to try to beat out other would-be buyers.

When the appraiser comes in, they look at things a bit more objectively. Their job is to assess the inherent value of the home, so they’re going to study the facts. Dustin Harris, Appraiser Coach, drives this point home:

“It’s important for everyone to understand that the appraiser’s job in the end is to remain that unbiased third party, to truly tell the client what that home is worth in the current market, regardless of what decisions have been made on the price side of things.”

In simple terms, while homebuyers may be willing to pay more, appraisers are there to assess the market value of the home. Their goal is to make sure the lender isn’t loaning more money than the home is worth. It’s objective, rather than emotional.

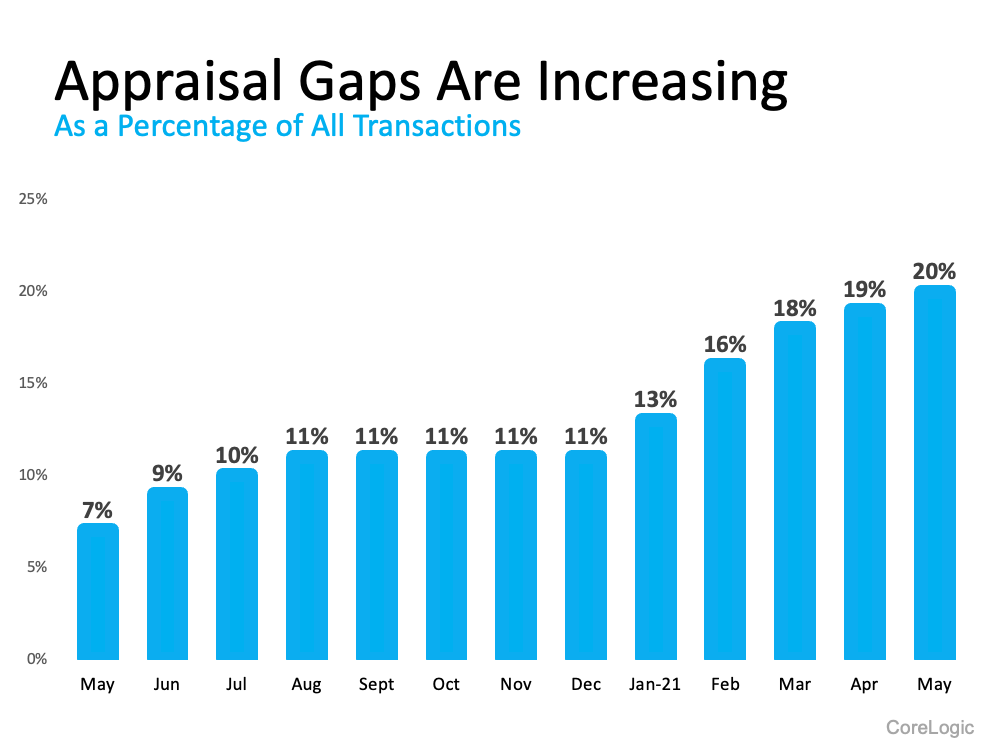

In a highly competitive market like today’s, having a discrepancy between the two numbers isn’t unusual. Here’s a look at the increasing rate of appraisal gaps, according to data from CoreLogic (see graph below):

Ultimately, knowledge is power. The best thing you can do is understand appraisal gaps may impact your transaction if you’re buying or selling. If you do encounter an appraisal below your contract price, know that in today’s sellers’ market, the most common approach is for the seller to ask the buyer to make up the difference in price. Buyers, be prepared to bring extra money to the table if you really want the home.

Above all else, lean on your real estate agent. Whether you’re a buyer or seller, your trusted advisor is your ally if you come up against an appraisal gap. We’ll help you understand your options and handle any additional negotiations that need to happen.

In today’s real estate market, it’s important to stay informed on the latest trends. Let’s connect so you have an ally to help you navigate an appraisal gap to get the best possible outcome.

There are many non-financial benefits of buying your own home. However, today’s headlines seem to be focusing primarily on the financial aspects of homeownership – specifically affordability. Many articles are making the claim that it’s not affordable to buy a home in today’s market, but that isn’t the case.

Today’s buyers are spending approximately 20% of their income on their monthly mortgage payments. According to The Essential Guide to Creating a Homebuying Budget from Freddie Mac, the 20% of income that purchasers are currently paying is well within the 28% guideline suggested:

“Most lenders agree that you should spend no more than 28% of your gross monthly income on a mortgage payment (including principal, interest, taxes and insurance).”

So why is there so much talk about challenges regarding affordability?

Since home prices are rising, it’s true that homes are less affordable than they have been since the housing crash fifteen years ago. Headlines making these claims aren’t incorrect; they just don’t tell the whole story. To paint the full picture, you have to look at how today stacks up with historical data. A closer analysis of affordability going further back in time reveals that homes today are more affordable than any time from 1975 to 2005.

Despite that, the chatter about affordability is pushing some buyers to the sidelines. They don’t feel comfortable knowing someone else got a better deal a year ago.

In a recent post, Odeta Kushi, Deputy Chief Economist at First American, offers a different take on the financial components of housing affordability. Kushi proposes we should at least consider the impact equity build-up has on the affordability equation, stating:

“For those trying to buy a home, rapid house price appreciation can be intimidating and makes the purchase more expensive. However, once the home is purchased, appreciation helps build equity in the home, and becomes a benefit rather than a cost. When accounting for the appreciation benefit in our rent versus own analysis, it was cheaper to own in every one of the top 50 markets.”

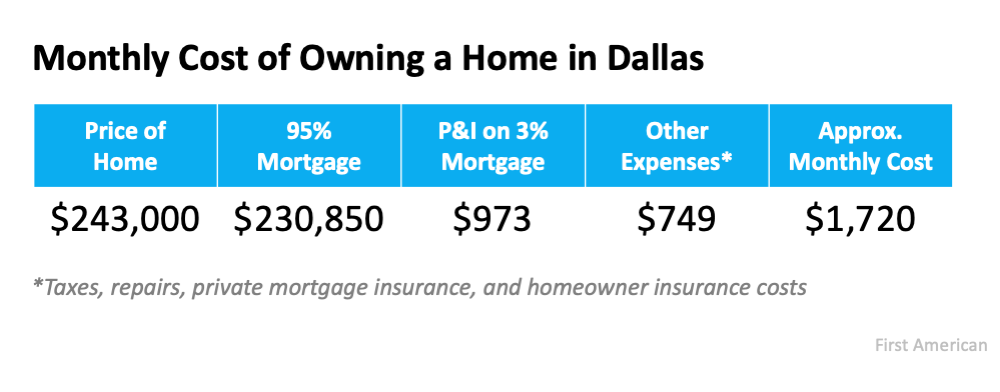

Let’s look at an example. In the above-mentioned post, Kushi examines the rent versus buy situation in Dallas, Texas. Kushi chose Dallas because home prices there sit near the median of the top 50 markets in the nation.

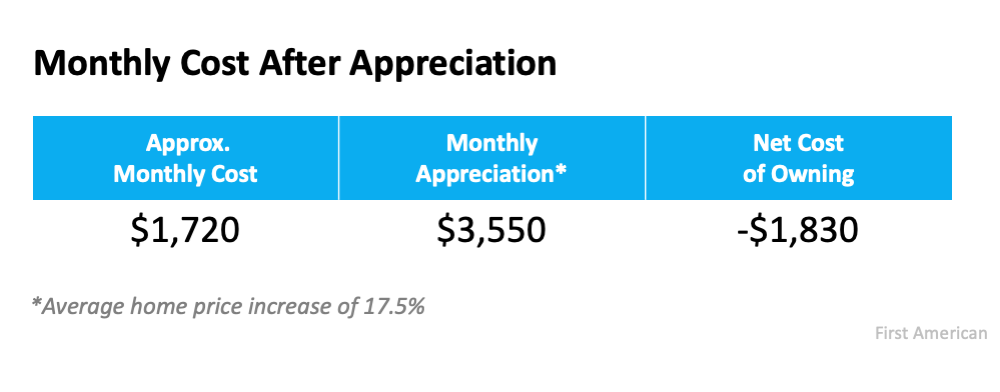

Kushi first calculates the monthly mortgage payment on a median-priced home with a 5% down payment and a mortgage rate of 3% (see chart below): Kushi then takes the monthly cost and subtracts the appreciation the home had over the previous twelve months. The average house price in Dallas increased 17.5% in the second quarter of 2021 compared to last year (this is in line with the national pace). That equates to an equity benefit of approximately $3,550 each month if the pace remains the same (see chart below):

Kushi then takes the monthly cost and subtracts the appreciation the home had over the previous twelve months. The average house price in Dallas increased 17.5% in the second quarter of 2021 compared to last year (this is in line with the national pace). That equates to an equity benefit of approximately $3,550 each month if the pace remains the same (see chart below): We can see the equity gained each month was greater than the monthly mortgage payment, resulting in a negative cost to own. The buyer could build their net worth by $1,830 each month – after paying their mortgage.

We can see the equity gained each month was greater than the monthly mortgage payment, resulting in a negative cost to own. The buyer could build their net worth by $1,830 each month – after paying their mortgage.

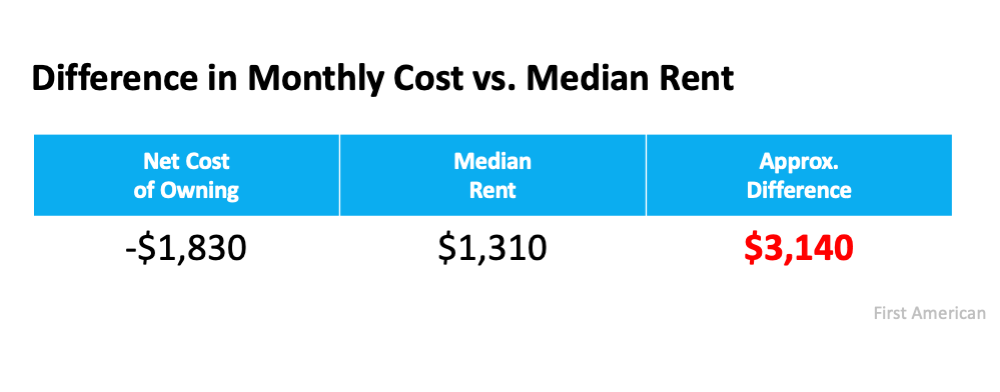

Kushi then compares the monthly cost of owning to the cost of renting (see chart below): When adding equity build-up into the equation, the cost of renting is $3,140 more expensive than owning. Again, the First American analysis shows that it’s less expensive to own in each of the top 50 markets in the country when including the equity component.

When adding equity build-up into the equation, the cost of renting is $3,140 more expensive than owning. Again, the First American analysis shows that it’s less expensive to own in each of the top 50 markets in the country when including the equity component.

If you’re on the fence about whether to buy or rent right now, let’s connect so we can determine if the equity increase in our local market should impact your decision.

Give us a call at 870-425-4300.

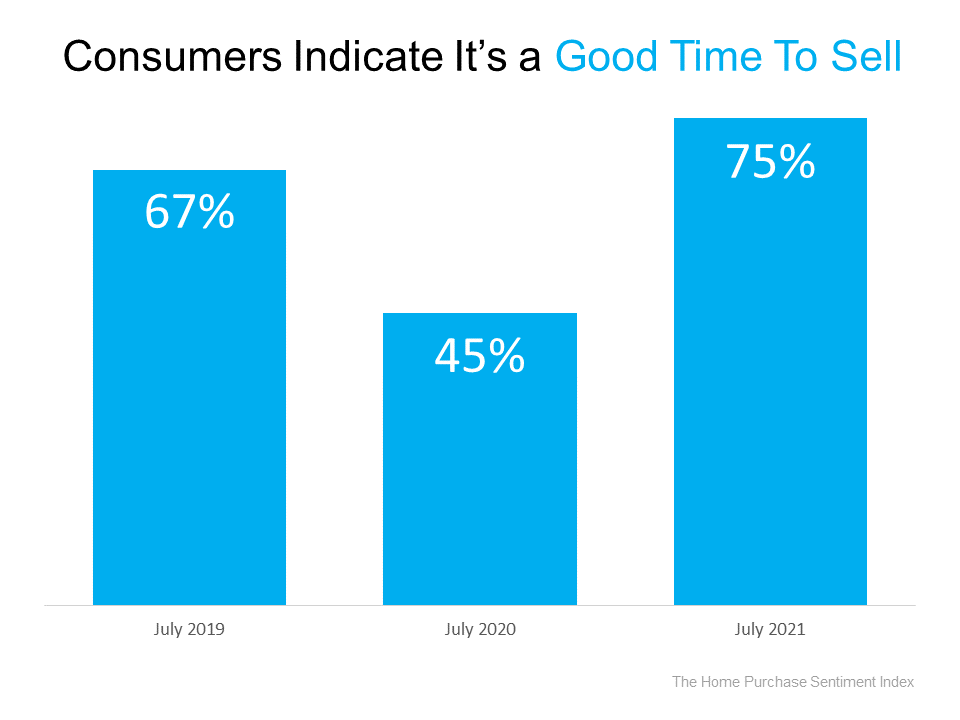

If you’re trying to decide whether or not to sell your house, this is the time to think seriously about making a move. Fannie Mae’s recent Home Purchase Sentiment Index (HPSI) reveals the number of respondents who say it’s a good time to sell is higher now than it was over the past few summers (see graph below). Today, the majority of consumers, 75 percent, say it’s a good time to sell a house.

The higher good time to sell sentiment has to do with today’s market conditions, specifically low housing supply and high buyer demand. In the simplest terms, we don’t have enough houses available for sale to meet buyer demand.

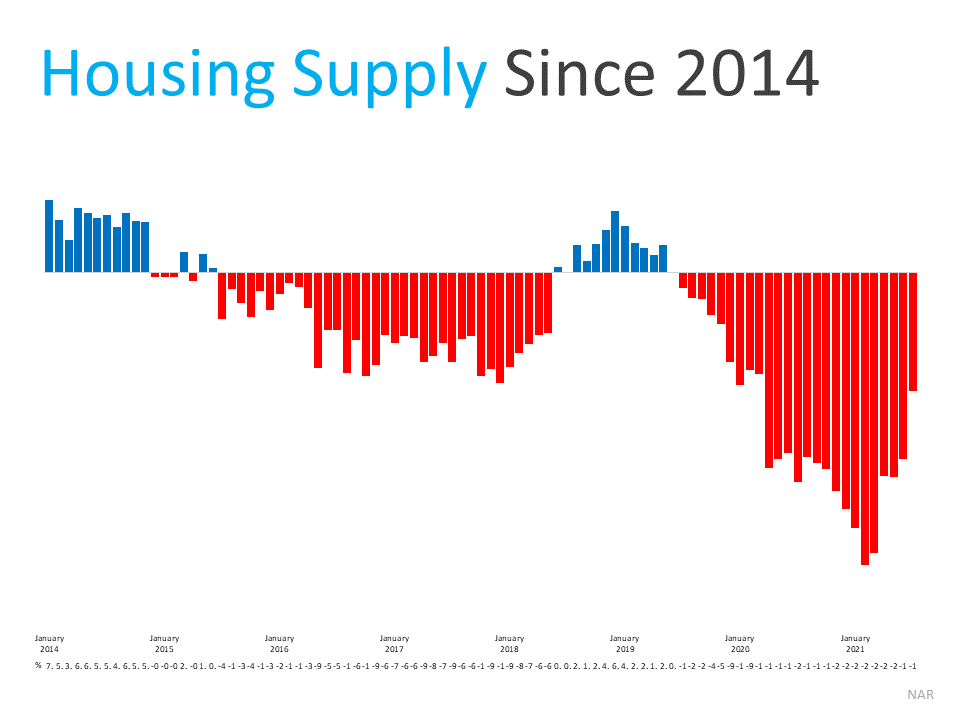

According to the latest data from the National Association of Realtors (NAR), we’re still firmly in a sellers’ market because housing supply is well below a balanced norm (shown in the graph below). Clearly, the scales are tipped in a seller’s favor today. But while housing supply is undeniably low, the right side of the graph shows how the inventory situation is improving little by little each month as more sellers list their homes for sale.

Clearly, the scales are tipped in a seller’s favor today. But while housing supply is undeniably low, the right side of the graph shows how the inventory situation is improving little by little each month as more sellers list their homes for sale.

As a seller, that means each month, buyers have more options to pick from. By extension, that means your house may get less buyer attention with time. Danielle Hale, Chief Economist for realtor.com, explains it like this:

“More homeowners continue to list homes for sale compared to a year ago… Notably, while new listings continue to lag behind a more ‘normal’ 2019 pace, the gap is shrinking. Even though homes continue to sell quickly thanks to high demand and limited supply, new listings are subtly shifting the balance of market conditions in favor of buyers.”

If you’ve been waiting for the perfect time to sell, there may not be a better chance than right now. Inventory is gradually increasing each month, so selling sooner rather than later will help you maximize your home’s potential.

If you’re planning to sell your house, 2021 is still the year to do it. The unique mix of low supply and high demand won’t last forever. Let’s connect to discuss what you need to do now to sell your house and take advantage of this sellers’ market.

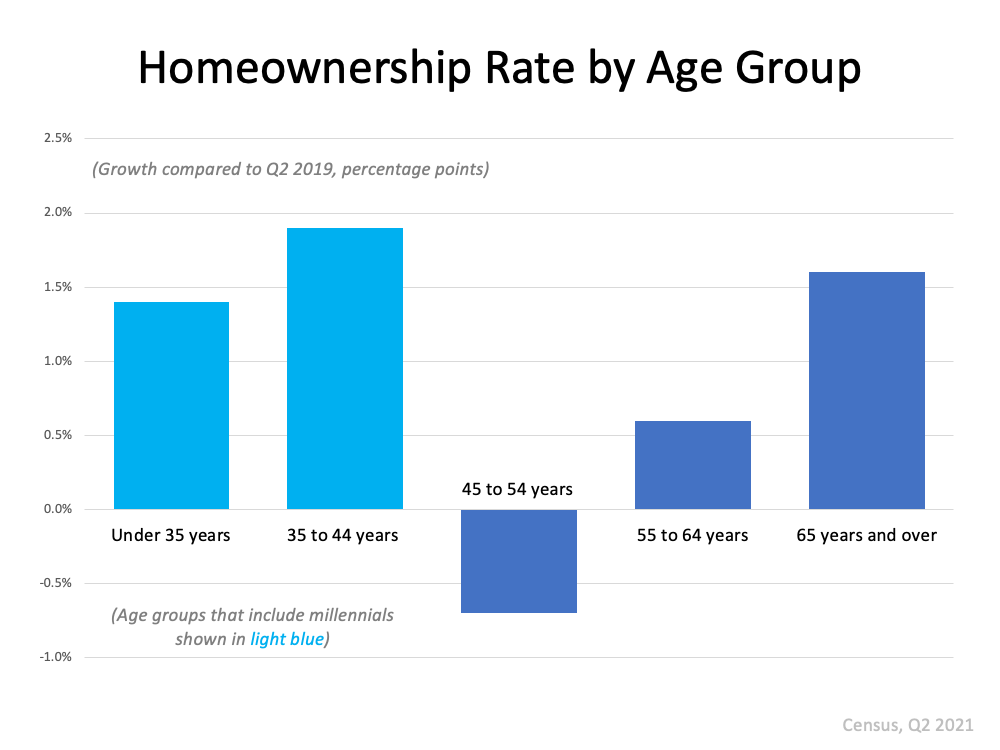

There’s a common misconception that younger generations aren’t interested in homeownership. Many people point to the fact that millennials put off purchasing their first home as a reason for this belief.

Odeta Kushi, Deputy Chief Economist for First American, explains why millennials have put off certain milestones linked to homeownership. Those delays led to their homeownership rates trailing slightly behind older generations:

“Historically, millennials have delayed the critical lifestyle choices often linked to buying a first home, including getting married and having children, in order to further their education. This is clear in cross-generational comparisons of homeownership rates which show millennials lagging their generational predecessors.”

So, it’s partially true that some millennials have waited on homeownership to focus on other things in their lives – and that’s impacting certain housing market trends.

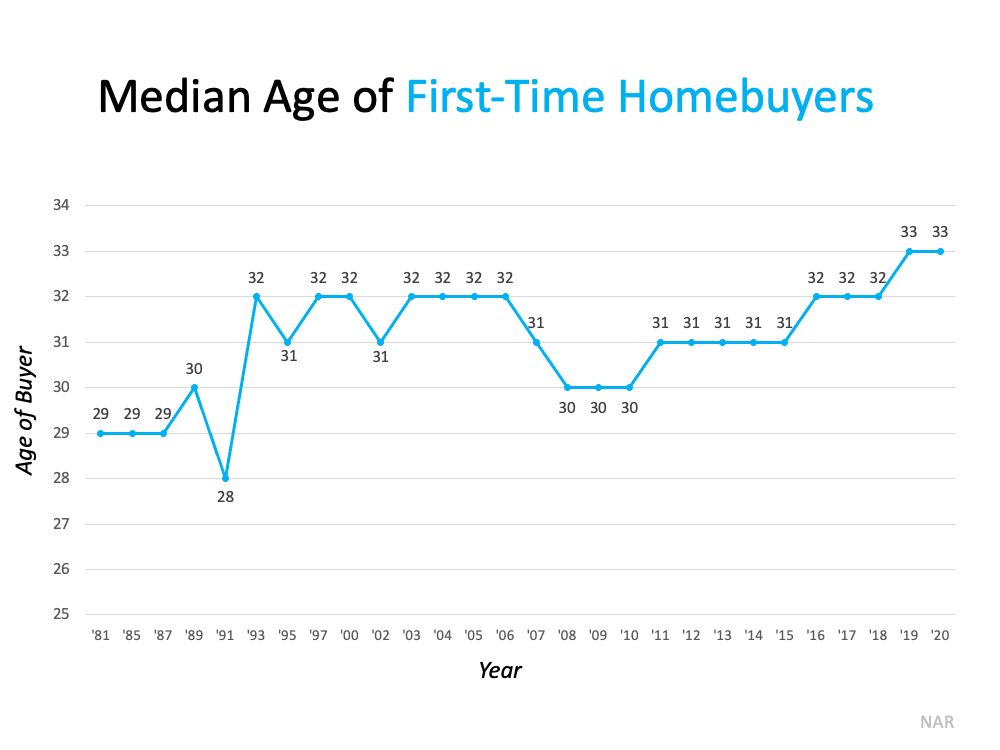

Data from the National Association of Realtors (NAR) indicates the average age of a first-time homebuyer is higher today than it’s been over the past 40 years. As the graph below shows, homebuyers today are purchasing their first home an average of 4 years later than people in the 1980s and early 1990s: But just because millennials are hitting certain milestones later in life doesn’t mean they’re not interested in becoming homeowners. The recent U.S. Census reveals a significant increase in homeownership rates for millennials and other young homebuyers.

But just because millennials are hitting certain milestones later in life doesn’t mean they’re not interested in becoming homeowners. The recent U.S. Census reveals a significant increase in homeownership rates for millennials and other young homebuyers. As the graph above shows, millennials are entering the market in full force, and their share of the market is growing. Based on the data, the belief that younger generations don’t want to buy homes is a misconception. In fact, the recent Capital Market Outlook report from Merrill-Lynch further drives home this point, as it specifically mentions the effect millennials are having on demand:

As the graph above shows, millennials are entering the market in full force, and their share of the market is growing. Based on the data, the belief that younger generations don’t want to buy homes is a misconception. In fact, the recent Capital Market Outlook report from Merrill-Lynch further drives home this point, as it specifically mentions the effect millennials are having on demand:

“Demand is very strong because the biggest demographic cohort in history is moving through the household-formation and peak home-buying stages of its life cycle.”

Kushi is following the trend of millennial homeownership and puts it more simply, saying:

“. . . it’s clear that younger households (millennials!) are driving homeownership growth.”

As the largest generation, millennials’ impact on the market is growing as more and more people from that generation reach homebuying age – and Generation Z isn’t far behind, either. That means younger generations will likely continue to drive demand in the housing market for years to come.

If you’re a member of a younger generation and interested in purchasing a home, you’re not alone. Many of your peers are on their path to homeownership, too. Let’s connect today and discuss what you can do to accomplish your homebuying goals.

Whether or not you’ve been following the real estate industry lately, there’s a good chance you’ve heard we’re in a serious sellers’ market. But what does that really mean? And why are conditions today so good for people who want to list their house?

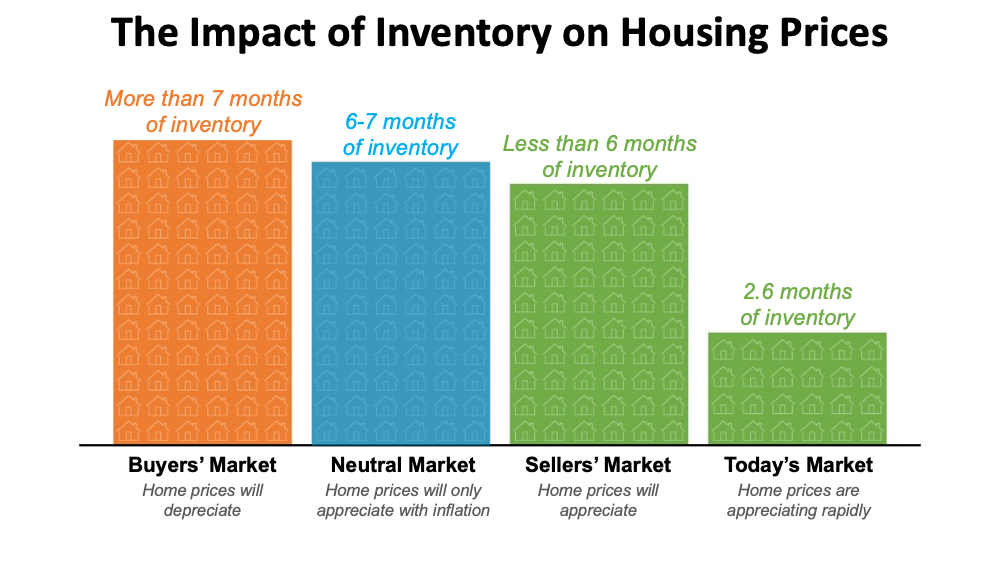

It starts with the number of houses available for sale. The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows housing supply is still astonishingly low. Today, we have a 2.6-month supply of homes at the current sales pace. Historically, a 6-month supply is necessary for a ‘normal’ or ‘neutral’ market in which there are enough homes available for active buyers (see graph below): When the supply of houses for sale is as low as it is right now, it’s much harder for buyers to find homes to purchase. That creates increased competition among purchasers which leads to more bidding wars. And if buyers know they may be entering a bidding war, they’re going to do their best to submit a very attractive offer. As this happens, home prices rise, and sellers are in the best position to negotiate deals that meet their ideal terms.

When the supply of houses for sale is as low as it is right now, it’s much harder for buyers to find homes to purchase. That creates increased competition among purchasers which leads to more bidding wars. And if buyers know they may be entering a bidding war, they’re going to do their best to submit a very attractive offer. As this happens, home prices rise, and sellers are in the best position to negotiate deals that meet their ideal terms.

Right now, there are many buyers who are ready, willing, and able to purchase a home. Low mortgage rates and the ongoing rise in remote work have prompted buyers to think differently about where they live – and they’re taking action. If you put your house on the market while supply is still low, it will likely get a lot of attention from competitive buyers.

Today’s ultimate sellers’ market holds great opportunities for homeowners ready to make a move. Listing your house now will maximize your exposure to serious buyers who will actively compete against each other to purchase it. Let’s connect to discuss how to jumpstart the selling process. 870-425-4300

In the current sellers’ market, many homeowners wonder what, if anything, needs to be remodeled before they list their house. That’s where a trusted real estate professional comes in. They can help you think through today’s market conditions and how they impact what you should – and shouldn’t – renovate before selling.

Here are some considerations a professional will guide you through:

A more balanced market typically sees a 6-month supply of homes for sale. Above that, and we’re in a buyers’ market. Below that, and we’re in a sellers’ market. According to a recent report by the National Association of Realtors (NAR), our current supply of homes for sale, while rising, still remains solidly in sellers’ market territory:

“Unsold inventory sits at a 2.6-month supply at the current sales pace, modestly up from May’s 2.5-month supply but down from 3.9 months in June 2020.”

So, what’s that mean for you? If you’re a seller trying to decide whether or not to renovate, this is especially important because it’s indicative of buyer behavior. When there aren’t enough homes for sale, buyers may be more willing to purchase a home that doesn’t meet all their needs and renovate it themselves later.

You don’t want to spend time and money on a project that isn’t worth the cost or is too niche design-wise for some homebuyers. According to an article by Renofi.com, basing home updates on what’s trendy right now can be a costly mistake:

“The last thing you as a homeowner want to do is center your home design around a passing fad – even worse, one thats design quality won’t last a good while.”

Before making any decisions, talk to your real estate advisor. They have insight into what other sellers are doing before listing their homes and how buyers are reacting to those upgrades. Don’t spend the time and money to be trendy – if your buyer wants to upgrade to the newest fad later, they can.

If you have already completed some renovations on your house, you’re not alone. The pandemic kept people at home last year, and during that time, many homeowners completed some home improvement projects. HomeAdvisor’s 2021 State of Home Spending Report found:

“35% of households that completed an improvement project undertook some type of interior painting, while 31% completed a bathroom remodel and 26% installed new flooring.”

Let your real estate professional know if you fall in this category. They can highlight any recent upgrades you’ve made in your house’s listing.

When it comes to renovations, your return-on-investment should be top of mind. Let’s connect today to talk through any upgrades you’ve already made and to find out what you should prioritize before you sell to maximize your house’s potential.

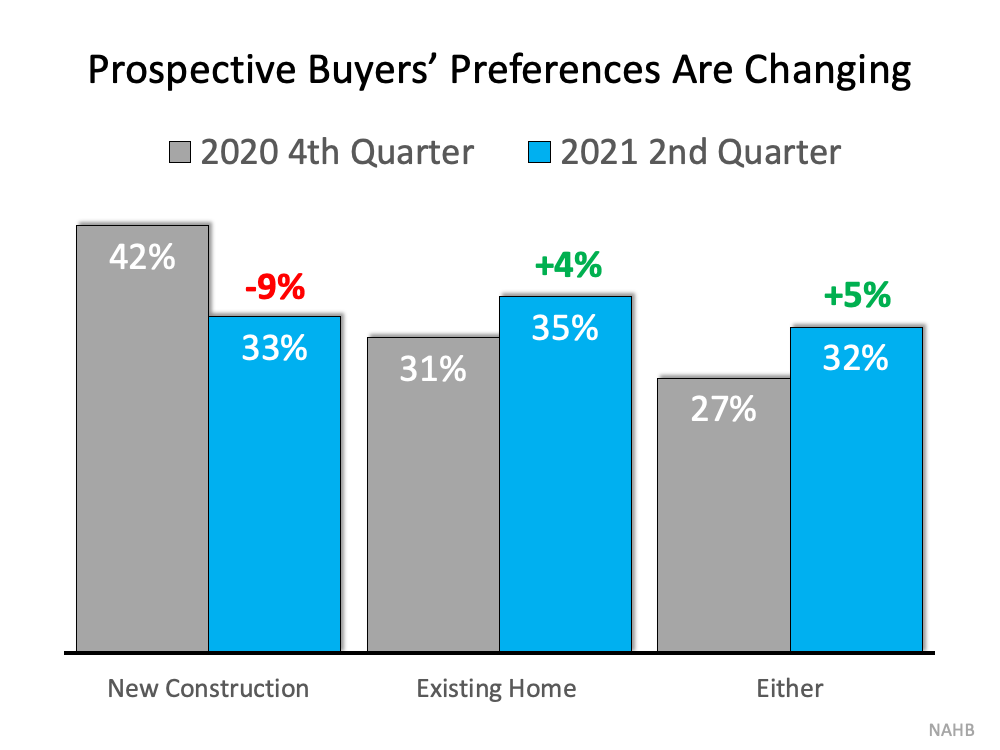

In April, the National Association of Home Builders (NAHB) posted an article, Home Buyers’ Preferences Shift Towards New Construction, which reported:

“60% of people who were looking to buy a home in 2020 said they’d prefer new construction to an existing home.”

The latest Consumer Confidence Survey reveals the percentage of Americans planning to buy a home in the next six months is virtually the same as it was back in March. However, the percentage that plan to buy a newly constructed home is lower for that same period.

NAHB confirms this sentiment in their latest Housing Trends Report. The organization explains that existing homes are now the top preference among today’s buyers. Here’s a breakdown of those findings:

There are several reasons why buyer preference is shifting. Here are two that impact purchasers looking to move in now:

If you’re a homeowner looking to sell, your house is more attractive to a greater number of buyers as compared to earlier in the year. This might be the time for us to connect to discuss the possibility.

According to recent data from realtor.com, median rental prices have reached their highest point ever recorded in many areas across the country. The report found rents rose by 8.1% from the same time last year. As it notes:

“Beyond simply recovering to pre-pandemic levels, rents across the country are surging. Typically, rents fluctuate less than 1% from month to month. In May and June, rents increased by 3.0% and 3.2% from each month to the next.”

If you’re a renter concerned about rising prices, now may be the time to consider purchasing a home.

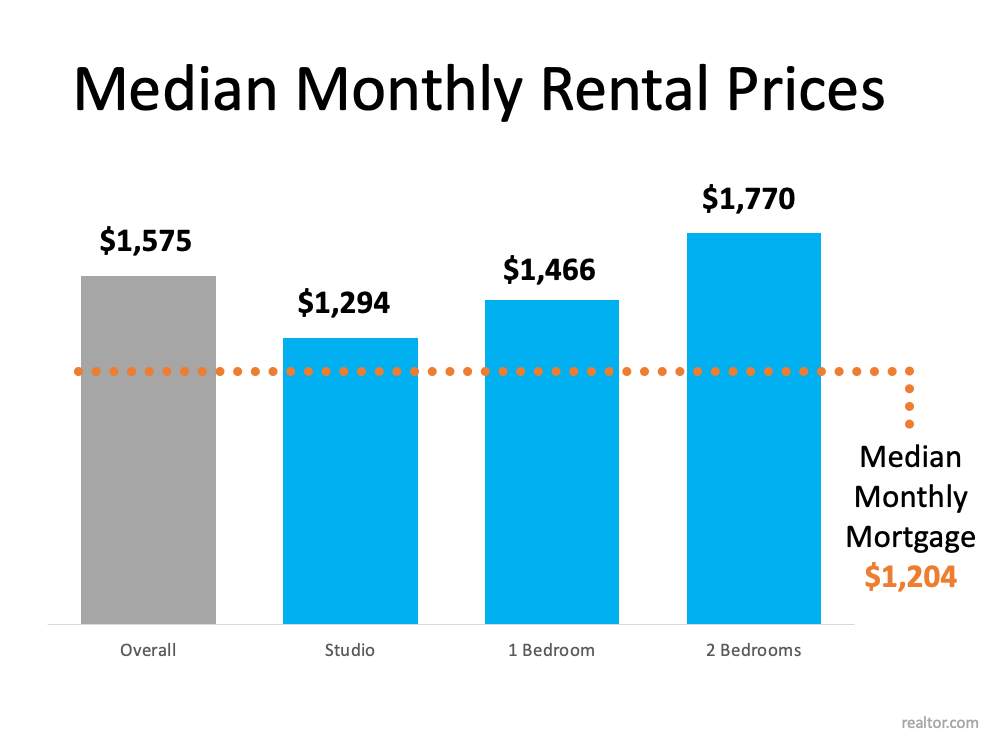

When you weigh your options of whether to buy a home or continue renting, how much you’ll pay each month is likely top of mind. According to the National Association of Realtors (NAR), monthly mortgage payments are rising, but they’re still significantly lower than the typical rental payment. NAR indicates the latest data on homes closed shows the median monthly mortgage payment is $1,204.

By contrast, the median national rent is $1,575 according to the most current data provided by realtor.com. In other words, buyers who recently purchased a home locked in a monthly payment that is, on average, $371 lower than what renters pay today (see graph below):

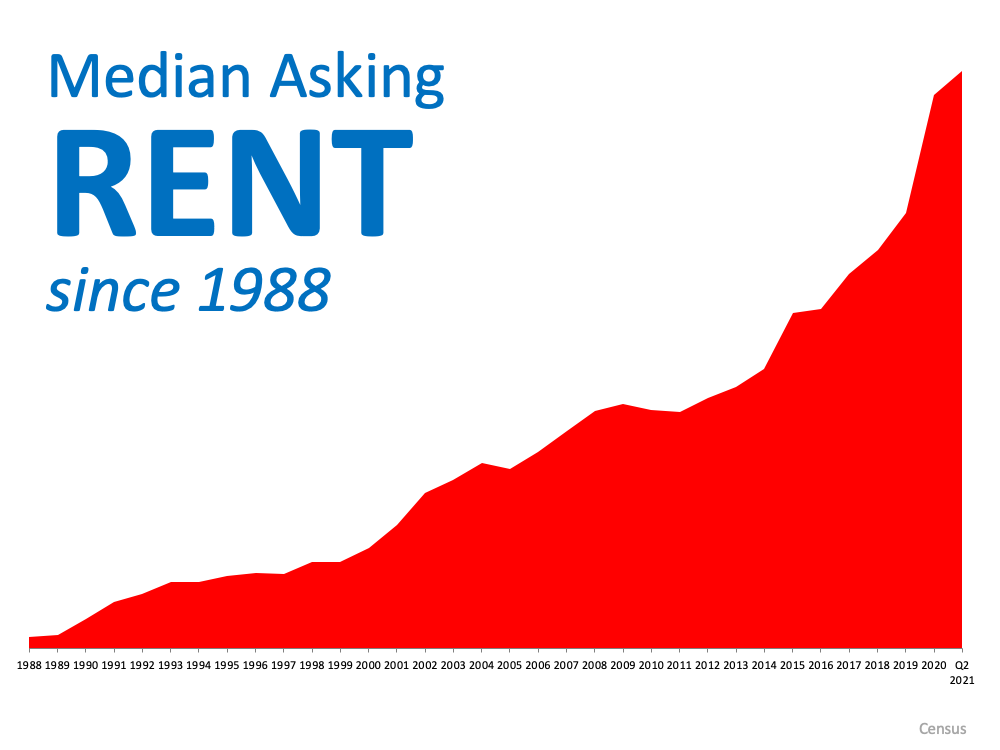

The difference in monthly housing costs when comparing renting and homebuying today is significant, but many would-be homebuyers wonder about the future of rental prices. If we look to historical Census data as a reference, the median asking rent has risen consistently since 1988 (see graph below): The rise in rent over time clearly shows one of the major advantages homeownership has over renting: stable housing costs. Renters face increasing costs every year. When you purchase your home, your mortgage rate is locked in for 30 years, meaning your monthly payment stays the same over time. That gives you welcome peace of mind and predictability for many years ahead.

The rise in rent over time clearly shows one of the major advantages homeownership has over renting: stable housing costs. Renters face increasing costs every year. When you purchase your home, your mortgage rate is locked in for 30 years, meaning your monthly payment stays the same over time. That gives you welcome peace of mind and predictability for many years ahead.

With rents continuing to rise across the country, renters should consider if now is the right time to buy. There are multiple benefits to buying sooner rather than later. Let’s discuss your options so you can make your most powerful decision. Give any one of our agents a call at 870-425-4300 TODAY!